投资 投资 LY 2025-09-16 2026-03-25 前言 这篇帖子主要是用机器学习算法,以常见的量价因子为例,测试价格预测能力,涉及的量价因子如下:

价格趋势因子

移动平均类

SMA_5

SMA_10

SMA_20

EMA_5

EMA_10

EMA_20

动量指标

MACD

MACD_signal

MACD_hist

波动率因子

其他相关因子

volume

open_oi

close_oi

returns【收益率】

基础

图片中文乱码,懒得改了,不影响阅读

数据来源,可以参考这篇文章:金融数据采集 | FlyDay

必要库导入 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 import pandas as pdimport numpy as npimport matplotlib.pyplot as pltimport seaborn as snsfrom sklearn.model_selection import train_test_split, TimeSeriesSplit, GridSearchCVfrom sklearn.preprocessing import StandardScaler, MinMaxScalerfrom sklearn.metrics import mean_squared_error, mean_absolute_error, r2_scorefrom sklearn.linear_model import LinearRegression, Ridge, Lasso, ElasticNetfrom sklearn.ensemble import RandomForestRegressor, GradientBoostingRegressorfrom sklearn.svm import SVRfrom sklearn.neural_network import MLPRegressorfrom xgboost import XGBRegressorfrom lightgbm import LGBMRegressorfrom catboost import CatBoostRegressorimport warningswarnings.filterwarnings('ignore' ) plt.style.use('seaborn-v0_8' ) sns.set_palette("husl" ) %matplotlib inline

加载数据 1 2 3 4 5 file_path = "file/KQ_m_CZCE_SA_3m.csv" df = pd.read_csv(file_path) print ("数据形状:" , df.shape)print ("\n前5行数据:" )df.head()

数据形状: (10000, 12)

datetime

id

open

high

low

close

volume

open_oi

close_oi

symbol

duration

date

0

2023-04-20 10:30:00+08:00

90620.0

2224.0

2225.0

2217.0

2218.0

44242.0

879082.0

886347.0

KQ.m@CZCE.SA 180

2023-04-20

1

2023-04-20 10:33:00+08:00

90621.0

2218.0

2220.0

2213.0

2214.0

37043.0

886347.0

887119.0

KQ.m@CZCE.SA 180

2023-04-20

2

2023-04-20 10:36:00+08:00

90622.0

2214.0

2216.0

2207.0

2210.0

55160.0

887119.0

886485.0

KQ.m@CZCE.SA 180

2023-04-20

3

2023-04-20 10:39:00+08:00

90623.0

2210.0

2211.0

2204.0

2205.0

42947.0

886485.0

887544.0

KQ.m@CZCE.SA 180

2023-04-20

4

2023-04-20 10:42:00+08:00

90624.0

2205.0

2208.0

2200.0

2202.0

48951.0

887544.0

891117.0

KQ.m@CZCE.SA 180

2023-04-20

数据基本信息 1 2 3 4 5 6 print ("数据基本信息:" )print (df.info())print ("\n缺失值统计:" )print (df.isnull().sum ())print ("\n描述性统计:" )df.describe()

1 2 3 4 数据基本信息: <class 'pandas.core.frame.DataFrame'> RangeIndex: 10000 entries, 0 to 9999 Data columns (total 12 columns):

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 # Column Non-Null Count Dtype --- ------ -------------- ----- 0 datetime 10000 non-null object 1 id 10000 non-null float64 2 open 10000 non-null float64 3 high 10000 non-null float64 4 low 10000 non-null float64 5 close 10000 non-null float64 6 volume 10000 non-null float64 7 open_oi 10000 non-null float64 8 close_oi 10000 non-null float64 9 symbol 10000 non-null object 10 duration 10000 non-null int64 11 date 10000 non-null object dtypes: float64(8), int64(1), object(3) memory usage: 937.6+ KB None 缺失值统计: datetime 0 id 0 open 0 high 0 low 0 close 0 volume 0 open_oi 0 close_oi 0 symbol 0 duration 0 date 0 dtype: int64

描述性统计:

id

open

high

low

close

volume

open_oi

close_oi

duration

count

10000.00000

10000.000000

10000.000000

10000.000000

10000.000000

10000.000000

1.000000e+04

1.000000e+04

10000.0

mean

95619.50000

1798.731600

1801.590100

1795.792400

1798.714400

18270.753800

1.073193e+06

1.073204e+06

180.0

std

2886.89568

192.727222

192.958489

192.477165

192.697244

16468.048484

1.713484e+05

1.713394e+05

0.0

min

90620.00000

1511.000000

1517.000000

1508.000000

1511.000000

817.000000

5.486800e+05

5.486800e+05

180.0

25%

93119.75000

1651.000000

1654.000000

1648.000000

1651.000000

8140.750000

9.515280e+05

9.515445e+05

180.0

50%

95619.50000

1708.000000

1711.000000

1704.000000

1708.000000

13232.500000

1.114078e+06

1.114078e+06

180.0

75%

98119.25000

1953.000000

1956.000000

1948.000000

1953.000000

22584.750000

1.180854e+06

1.180854e+06

180.0

max

100619.00000

2248.000000

2251.000000

2242.000000

2248.000000

255318.000000

1.379724e+06

1.379724e+06

180.0

将datetime转换为日期时间类型并设置为索引 1 2 3 4 5 6 df['datetime' ] = pd.to_datetime(df['datetime' ]) df.set_index('datetime' , inplace=True ) df.sort_index(inplace=True ) print (f"数据时间范围: {df.index.min ()} 到 {df.index.max ()} " )

数据时间范围: 2023-04-20 10:30:00+08:00 到 2023-08-28 22:12:00+08:00

数据预处理和特征工程 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 df['target' ] = df['close' ].shift(-1 ) df = df.iloc[:-1 ] def add_technical_indicators (df ): df['SMA_5' ] = df['close' ].rolling(window=5 ).mean() df['SMA_10' ] = df['close' ].rolling(window=10 ).mean() df['SMA_20' ] = df['close' ].rolling(window=20 ).mean() df['EMA_5' ] = df['close' ].ewm(span=5 ).mean() df['EMA_10' ] = df['close' ].ewm(span=10 ).mean() df['EMA_20' ] = df['close' ].ewm(span=20 ).mean() delta = df['close' ].diff() gain = (delta.where(delta > 0 , 0 )).rolling(window=14 ).mean() loss = (-delta.where(delta < 0 , 0 )).rolling(window=14 ).mean() rs = gain / loss df['RSI' ] = 100 - (100 / (1 + rs)) exp12 = df['close' ].ewm(span=12 ).mean() exp26 = df['close' ].ewm(span=26 ).mean() df['MACD' ] = exp12 - exp26 df['MACD_signal' ] = df['MACD' ].ewm(span=9 ).mean() df['MACD_hist' ] = df['MACD' ] - df['MACD_signal' ] df['BB_middle' ] = df['close' ].rolling(window=20 ).mean() bb_std = df['close' ].rolling(window=20 ).std() df['BB_upper' ] = df['BB_middle' ] + (bb_std * 2 ) df['BB_lower' ] = df['BB_middle' ] - (bb_std * 2 ) df['BB_width' ] = (df['BB_upper' ] - df['BB_lower' ]) / df['BB_middle' ] df['returns' ] = df['close' ].pct_change() df['volatility' ] = df['returns' ].rolling(window=20 ).std() return df df = add_technical_indicators(df) df.dropna(inplace=True ) print ("添加技术指标后的数据形状:" , df.shape)df[['close' , 'SMA_5' , 'SMA_10' , 'RSI' , 'MACD' , 'target' ]].head()

添加技术指标后的数据形状: (9958, 28)

datetime

close

SMA_5

SMA_10

RSI

MACD

target

2023-04-20 14:30:00+08:00

2225.0

2225.0

2224.4

50.000000

0.067594

2220.0

2023-04-20 14:33:00+08:00

2220.0

2224.8

2223.7

40.909091

-0.275750

2219.0

2023-04-20 14:36:00+08:00

2219.0

2224.0

2222.8

41.860465

-0.606698

2218.0

2023-04-20 14:39:00+08:00

2218.0

2222.2

2222.1

40.909091

-0.925325

2218.0

2023-04-20 14:42:00+08:00

2218.0

2220.0

2222.0

29.729730

-1.162220

2218.0

选择特征列 1 2 3 4 5 6 7 8 9 10 11 feature_columns = ['open' , 'high' , 'low' , 'close' , 'volume' , 'open_oi' , 'close_oi' , 'SMA_5' , 'SMA_10' , 'SMA_20' , 'EMA_5' , 'EMA_10' , 'EMA_20' , 'RSI' , 'MACD' , 'MACD_signal' , 'MACD_hist' , 'BB_middle' , 'BB_upper' , 'BB_lower' , 'BB_width' , 'returns' , 'volatility' ] X = df[feature_columns] y = df['target' ] print ("特征矩阵形状:" , X.shape)print ("目标变量形状:" , y.shape)

特征矩阵形状: (9958, 23)

1 2 3 4 5 6 7 # 对于时间序列数据,我们按时间顺序划分训练集和测试集 train_size = int(0.8 * len(X)) X_train, X_test = X.iloc[:train_size], X.iloc[train_size:] y_train, y_test = y.iloc[:train_size], y.iloc[train_size:] print("训练集大小:", X_train.shape) print("测试集大小:", X_test.shape)

训练集大小: (7983, 23)

1 2 3 4 scaler = StandardScaler() X_train_scaled = scaler.fit_transform(X_train) X_test_scaled = scaler.transform(X_test)

模型训练和评估 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 models = { 'Linear Regression' : LinearRegression(), 'Ridge Regression' : Ridge(alpha=1.0 ), 'Lasso Regression' : Lasso(alpha=0.1 ), 'Random Forest' : RandomForestRegressor(n_estimators=100 , random_state=42 ), 'Gradient Boosting' : GradientBoostingRegressor(n_estimators=100 , random_state=42 ), 'SVR' : SVR(kernel='rbf' , C=1.0 , gamma='scale' ), 'XGBoost' : XGBRegressor(n_estimators=100 , random_state=42 ), 'LightGBM' : LGBMRegressor(n_estimators=100 , random_state=42 ), 'CatBoost' : CatBoostRegressor(iterations=100 , verbose=0 , random_state=42 ) } results = {} for name, model in models.items(): print (f"训练 {name} ..." ) model.fit(X_train_scaled, y_train) y_pred = model.predict(X_test_scaled) mse = mean_squared_error(y_test, y_pred) mae = mean_absolute_error(y_test, y_pred) rmse = np.sqrt(mse) r2 = r2_score(y_test, y_pred) results[name] = { 'MSE' : mse, 'MAE' : mae, 'RMSE' : rmse, 'R2' : r2 } print (f"{name} - RMSE: {rmse:.4 f} , R2: {r2:.4 f} " ) results_df = pd.DataFrame(results).T results_df = results_df.sort_values('RMSE' ) results_df

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 训练 Linear Regression... Linear Regression - RMSE: 4.8202, R2: 0.9990 训练 Ridge Regression... Ridge Regression - RMSE: 4.8699, R2: 0.9990 训练 Lasso Regression... Lasso Regression - RMSE: 5.1683, R2: 0.9989 训练 Random Forest... Random Forest - RMSE: 12.8100, R2: 0.9930 训练 Gradient Boosting... Gradient Boosting - RMSE: 12.6408, R2: 0.9932 训练 SVR... SVR - RMSE: 34.2561, R2: 0.9500 训练 XGBoost... XGBoost - RMSE: 14.6063, R2: 0.9909 训练 LightGBM... [LightGBM] [Info] Auto-choosing col-wise multi-threading, the overhead of testing was 0.000541 seconds. You can set `force_col_wise=true` to remove the overhead. [LightGBM] [Info] Total Bins 5865 [LightGBM] [Info] Number of data points in the train set: 7983, number of used features: 23 [LightGBM] [Info] Start training from score 1824.969059 LightGBM - RMSE: 12.9541, R2: 0.9928 训练 CatBoost... CatBoost - RMSE: 15.7077, R2: 0.9895

MSE

MAE

RMSE

R2

Linear Regression

23.234569

3.077902

4.820225

0.999009

Ridge Regression

23.715960

3.081490

4.869903

0.998989

Lasso Regression

26.710834

3.342289

5.168253

0.998861

Gradient Boosting

159.790863

7.861443

12.640841

0.993188

Random Forest

164.096094

7.890666

12.810000

0.993004

LightGBM

167.809114

7.983772

12.954116

0.992846

XGBoost

213.343612

9.307866

14.606287

0.990905

CatBoost

246.730999

10.522483

15.707673

0.989481

SVR

1173.478480

24.779806

34.256072

0.949972

模型性能可视化 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 # 绘制模型性能比较 fig, axes = plt.subplots(2, 2, figsize=(15, 10)) # RMSE比较 results_df['RMSE'].plot(kind='bar', ax=axes[0, 0], color='skyblue') axes[0, 0].set_title('模型RMSE比较') axes[0, 0].set_ylabel('RMSE') axes[0, 0].tick_params(axis='x', rotation=45) # R²比较 results_df['R2'].plot(kind='bar', ax=axes[0, 1], color='lightgreen') axes[0, 1].set_title('模型R²比较') axes[0, 1].set_ylabel('R²') axes[0, 1].tick_params(axis='x', rotation=45) # MAE比较 results_df['MAE'].plot(kind='bar', ax=axes[1, 0], color='lightcoral') axes[1, 0].set_title('模型MAE比较') axes[1, 0].set_ylabel('MAE') axes[1, 0].tick_params(axis='x', rotation=45) # MSE比较 results_df['MSE'].plot(kind='bar', ax=axes[1, 1], color='gold') axes[1, 1].set_title('模型MSE比较') axes[1, 1].set_ylabel('MSE') axes[1, 1].tick_params(axis='x', rotation=45) plt.tight_layout() plt.show()

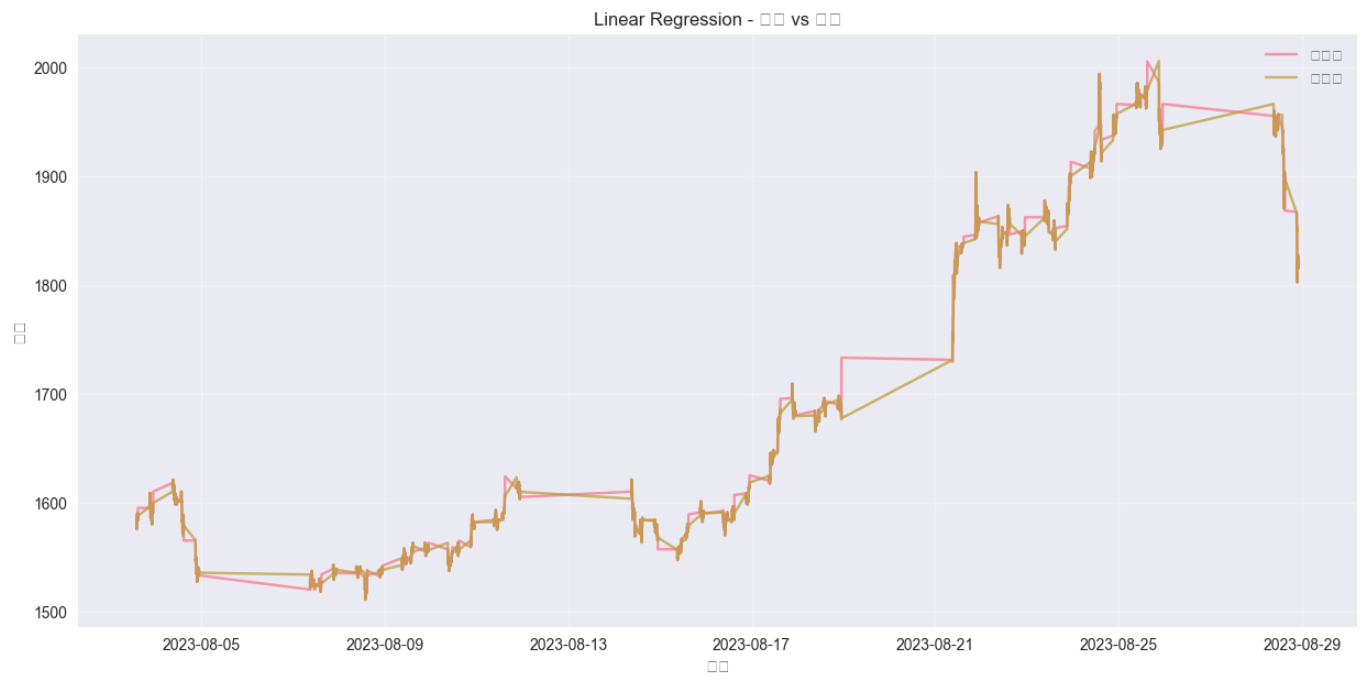

最佳模型预测结果可视化 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 best_model_name = results_df.index[0 ] print (f"最佳模型: {best_model_name} " )best_model = models[best_model_name] best_model.fit(X_train_scaled, y_train) y_pred = best_model.predict(X_test_scaled) plt.figure(figsize=(15 , 7 )) plt.plot(y_test.index, y_test.values, label='实际值' , alpha=0.7 ) plt.plot(y_test.index, y_pred, label='预测值' , alpha=0.7 ) plt.title(f'{best_model_name} - 预测 vs 实际' ) plt.xlabel('时间' ) plt.ylabel('价格' ) plt.legend() plt.grid(True , alpha=0.3 ) plt.show() residuals = y_test - y_pred plt.figure(figsize=(12 , 6 )) plt.scatter(y_pred, residuals, alpha=0.5 ) plt.axhline(y=0 , color='r' , linestyle='--' ) plt.title('残差图' ) plt.xlabel('预测值' ) plt.ylabel('残差' ) plt.grid(True , alpha=0.3 ) plt.show()

特征重要性分析(对于树模型) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 if hasattr (best_model, 'feature_importances_' ): feature_importance = pd.DataFrame({ 'feature' : feature_columns, 'importance' : best_model.feature_importances_ }) feature_importance = feature_importance.sort_values('importance' , ascending=False ) plt.figure(figsize=(12 , 8 )) plt.barh(feature_importance['feature' ][:15 ], feature_importance['importance' ][:15 ]) plt.title('Top 15 特征重要性' ) plt.xlabel('重要性' ) plt.tight_layout() plt.show() elif hasattr (best_model, 'coef_' ): feature_importance = pd.DataFrame({ 'feature' : feature_columns, 'coefficient' : best_model.coef_ }) feature_importance = feature_importance.sort_values('coefficient' , key=abs , ascending=False ) plt.figure(figsize=(12 , 8 )) plt.barh(feature_importance['feature' ][:15 ], feature_importance['coefficient' ][:15 ]) plt.title('Top 15 特征系数(绝对值)' ) plt.xlabel('系数值' ) plt.tight_layout() plt.show()

时间序列交叉验证 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 tscv = TimeSeriesSplit(n_splits=5 ) model = GradientBoostingRegressor(n_estimators=100 , random_state=42 ) cv_scores = [] for train_index, test_index in tscv.split(X): X_train_cv, X_test_cv = X.iloc[train_index], X.iloc[test_index] y_train_cv, y_test_cv = y.iloc[train_index], y.iloc[test_index] X_train_cv_scaled = scaler.fit_transform(X_train_cv) X_test_cv_scaled = scaler.transform(X_test_cv) model.fit(X_train_cv_scaled, y_train_cv) y_pred_cv = model.predict(X_test_cv_scaled) score = r2_score(y_test_cv, y_pred_cv) cv_scores.append(score) print ("交叉验证R²分数:" , cv_scores)print ("平均R²分数:" , np.mean(cv_scores))print ("R²分数标准差:" , np.std(cv_scores))plt.figure(figsize=(10 , 6 )) plt.plot(range (1 , 6 ), cv_scores, marker='o' ) plt.title('时间序列交叉验证性能' ) plt.xlabel('折数' ) plt.ylabel('R²分数' ) plt.grid(True , alpha=0.3 ) plt.show()

当然还可以超参数调优,这里就不继续了

模型部署和预测 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 # 使用最佳模型进行未来预测 def predict_future_price(model, last_known_data, scaler, steps=1): """ 使用训练好的模型预测未来价格 参数: model: 训练好的模型 last_known_data: 最后已知的数据点(DataFrame) scaler: 用于标准化的scaler steps: 预测步数 返回: predictions: 预测值列表 """ predictions = [] current_data = last_known_data.copy() for _ in range(steps): # 标准化当前数据 current_data_scaled = scaler.transform(current_data) # 预测下一步 next_price = model.predict(current_data_scaled)[0] predictions.append(next_price) # 更新当前数据(这里需要根据实际情况调整) # 在实际应用中,需要更复杂的逻辑来更新特征 current_data.iloc[0, 3] = next_price # 更新close价格 return predictions # 示例:使用最后一行数据进行预测 last_known = X.iloc[[-1]].copy() future_predictions = predict_future_price(best_model, last_known, scaler, steps=5) print("未来5期预测价格:", future_predictions)

1 未来5期预测价格: [np.float64(1832.2961094333193), np.float64(1840.6007680672349), np.float64(1847.2991579272611), np.float64(1852.7019599802757), np.float64(1857.0597639651191)]

具体对不对,能不能用,自己去查吧,哈哈哈~

相关文章